Business Description:

800 million monthly unique viewers globally

250 million hours viewed daily

Operates under 2 segments: US Networks and International Networks, each divided into advertising and distribution subsegments

65% of revenues in 2020 came from US Networks, 38% Advertising and 27% Distribution

35% of revenues in 2020 came from International Networks, 15% Advertising and 19% Distribution

Since shows are factual, expenses are limited compared to competitors with 2020 operating margins of 25% vs 18% for Viacom and Netflix and 2% for Disney (20% in 2019)

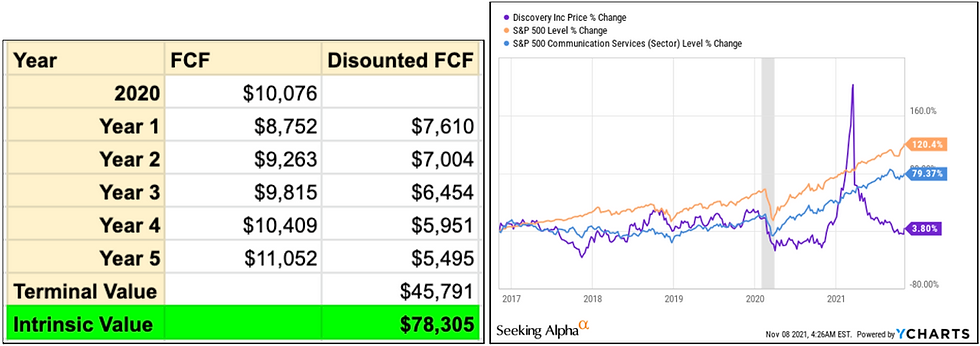

Stock crashed by 60% after a margin call from Archegos Capital

Merger with AT&T’s (NYSE:T) WarnerMedia

Structured as Reverse Morris Trust Transaction, whereby AT&T will spin off Warner Media which will then merge with Discovery

Discovery shareholders will own 29% of the new company

AT&T will receive $43 billion in a combination of cash, debt securities, and Warner’s retention of certain debt

Catalysts:

Recovery from pandemic

Content creation/acquisition is less expensive compared to competitors

Discovery+ ARPU expected to 3-4X US Networks Linear

Deal willl make Discovery more competitive with non-factual networks

Risks:

Streaming business is very competitive with Netflix, Disney+, Amazon Prime, Apple TV+ and others

Streaming business might be a cash flow drain in initial years

Cable Networks businesses are in decline

Concentrated business

Will no longer be a fully factual network

Synergy costs might be bigger than expected

Will take some of the debt of AT&T on balance sheet

AT&T shareholders unhappy about the dividend cut from the company

Financial Analysis:

Valuations:

My personal Biases:

4.0% of my portfolio

Assumptions for base case:

WarnerMedia was acquired by AT&T in 2018 for $85 billion

Below are the pro-forma financial estimates of WarnerMedia+Discovery for the last five years

Revenues in 2021 will slightly exceed 2019 level

US Network Revenues will grow by 12% annually from 2021-2025 (17% in the last five years) with operating margins of 35% (average of 45% in last five years)

International Network Revenues will grow by 4% annually from 2021-2025 (4% in the last five years) with operating margins of 10% (average of 12% in last five years)

4% of annual growth of WarnerMedia revenues

Operating margin of 25% for WarnerMedia

80% of operating income conversion in FCF

Discount rate of 15%

Terminal growth rate of 3%

Use P/FCF as exit multiples for 2025 (range of 5-33 in last 5 years)

Bull case 15% more than in base case and bear case 15% less

Shares outstanding doesn’t change

We will consider only prices for shares of Discovery, ignoring the new company (since we don’t know anything about pricing yet)

Conclusion

An intrinsic value of $78.3 billion for the new company means $22.7 billion for Discovery today

Undervalued with a market cap of $13.2 Billion for $22.7 Billion in intrinsic value in a conservative analysis

With a margin of safety, a fair value would be $20 billion

Exit multiples analysis shows an expected returns of 24% per year with limited downside of 20% and possible reward of over 400% in bull case

Comentarios